Broadcom (AVGO) Q2 Earnings Preview

I'm calling for shares of Broadcom to 3x over the next several years. Will the company stay on track and what does this mean for Nvidia and AMD stocks?

Broadcom AVGO 0.00%↑ reports Q2 earnings on Thursday June 5th.

Today I want to get you ready for the report by going over:

Wall Street Expectations

Conference Call

Technical Setup

Wall Street Estimates

Let’s start with Wall Street expectations for Q2. These are important and often can explain why a stock goes up or down after the report.

Q2 Revenue Estimates: $14.84B - $15.95B

Midpoint Consensus Estimate: $14.97B

Back in March Broadcom guided to $14.9B in revenue. Anything less would be a severe disappointment but unlikely due to the momentum around AI and the consistency of the software business.

$14.9B in revenue would represent roughly 20% revenue growth over the past year.

Aside from meeting the Q2 expectations, guidance for Q3 revenue must also achieve 20% growth.

Q3 Revenue Estimates: $15.32B - $16.72B

Midpoint Consensus Estimate: $15.77B

Wall Street sees Broadcom quarterly revenue peaking in the $17B - $20B range into 2026. If the company can convince analysts it can exceed those targets, shares of Broadcom will move higher.

Conference Call

CEO Hock Tan has been dropping bombs on the conference call lately.

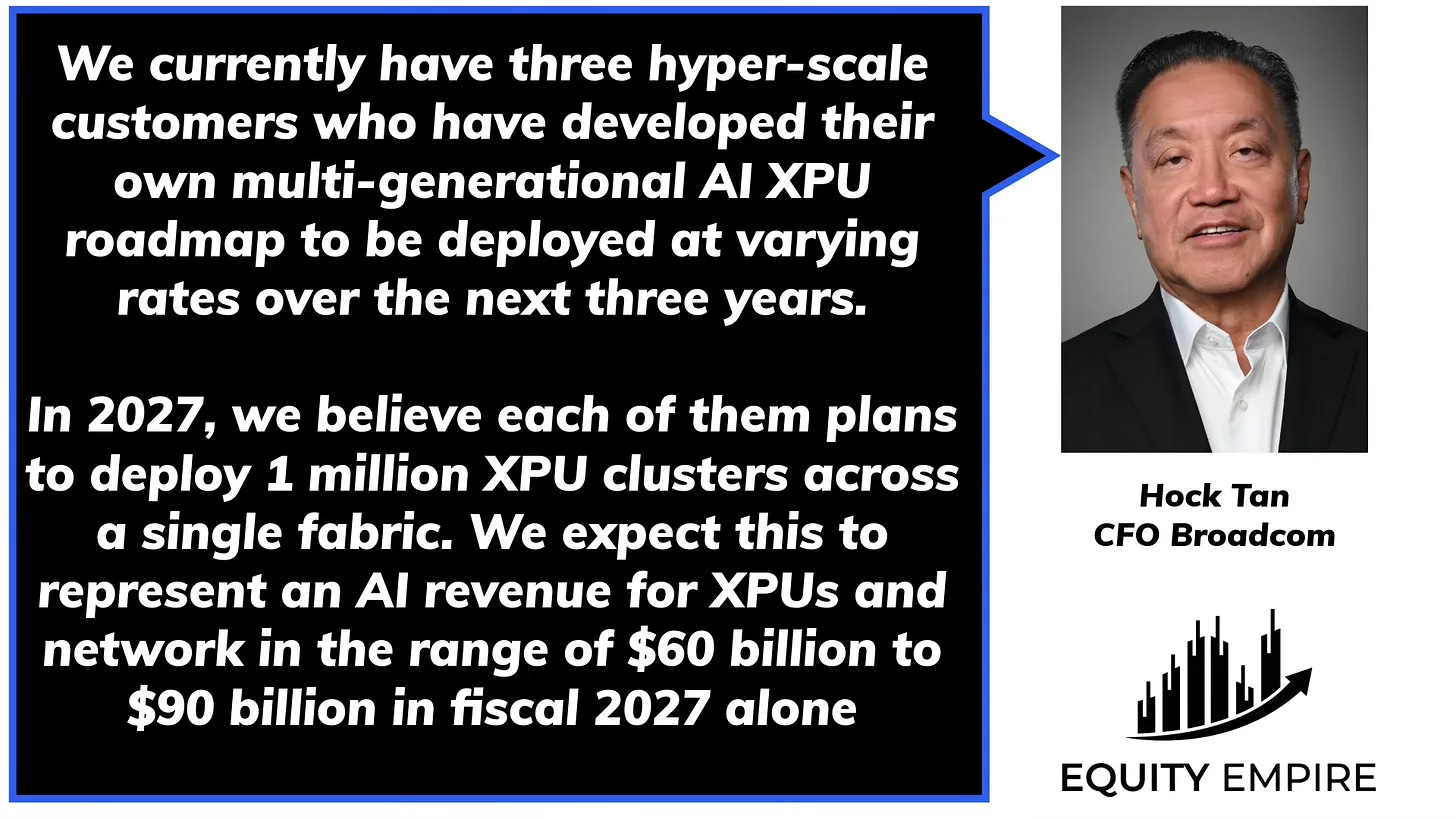

Last year, he revealed the company had 3 hyper-scale customers who wanted gigantic XPU clusters built. (XPU is just an industry term for a custom GPU).

It’s believed that Broadcom has 3 customers shipping in high volume at the current time.

One is obviously Google GOOGL 0.00%↑ GOOG 0.00%↑ which has been working with Broadcom for years.

The rumors around the semiconductor industry is Google has been trying to find an alternative supplier.

But it can’t find a company that can deliver the same performance and quality as Broadcom.

Keep in mind this is normal that companies try to find alternative suppliers. But in the semiconductor industry - it’s also normal for a company to be a generation (year) ahead of the competition.

This is the case with both Nvidia NVDA 0.00%↑ and Broadcom.

As long as they maintain this lead - they will capture significant revenue and maintain high gross margins.

Two other customers are already shipping in high volume, those are believed to be Meta META 0.00%↑ and ByteDance (TikTok).

As you might recall, Broadcom revealed that two additional hyper-scale customers were also in advanced discussions to launch large 1M+ clusters.

No way to know for certain who the additional 2 customers are, but it could be a combination of Apple $AAPL, Amazon $AMZN, Microsoft MSFT 0.00%↑, xAI (Elon Musk), or OpenAI (ChatGPT).

There’s no doubt I will be looking for updates on the current status and if potentially new customers emerge.

I wrote about all this in December if you need a refresher.

Keep in mind that Broadcom didn’t include the additional 2 customers in the $60B - $90B estimate. That estimate is primarily for Google, Meta and ByteDance spending in 2027.

Given that Google, Meta, and ByteDance could comfortably spend $60B - $90B between them in a year, Broadcom stock could comfortably obtain a $3T valuation if 5 customers do indeed come on board.

That would be a near triple from today price.

Basked into that valuation are things I don’t spend much time discussing including a ~ $30B/yr software business that prints 90% gross margins, and ~ $20B/yr semiconductor revenue not related to AI.

Nvidia & AMD

Nvidia is shipping Blackwell in large quantities in the current quarter and hyper scale customers are getting larger allocations. But Broadcom serves as a reliable alternative given AMD AMD 0.00%↑ missed the Q2 release window with its latest MI-series GPU.

For more on AMD, I wrote about its situation last week:

In the world of high-end data center GPUs, it’s currently a two (and a half) horse race between Nvidia and Broadcom … with AMD on the outside looking in until Q4.

Technical Setup

Technically, Broadcom shares are hitting overhead resistance at $248.

A break higher after earnings would be incredibly bullish.

Momentum traders would come in, likely driving shares into the $260s or higher.

A rejection at the $248 level is not cause for concern.

It’s normal for a stock to fight through the all-time highs.

Pull backs in Broadcom (given no fundamental damage) should be bought aggressively. I’ll save those levels for my premium subscribers, but it doesn’t take a chart wizard to locate those areas on the chart.

Make sure to join me Thursday June 5th at 6pm PST / 9pm EST for a special livestream where I will discuss Broadcom’s Q2 Earnings, conference call highlights and take questions!

YouTube Link: https://youtube.com/live/g2IhPq35lPI

The last one we did with Nvidia was a lot of fun and I look forward to seeing you all on Thursday.

Until then … stay safe and enjoy your week.

Colin

https://open.substack.com/pub/techitalt/p/broadcom-before-the-bell-why-im-still?r=5jmutn&utm_campaign=post&utm_medium=web&showWelcomeOnShare=true

Amen! Looking forward to this coverage.