Equity Empire: Blue Chip Buy Alert

This fashion brand has seen its stock dramatically underperform the last several years. After a series of missteps by outgoing CEO, the brand is poised to get its mojo back.

Today I have a Blue Chip Buy Alert for you all. For those of you familiar with my YouTube Channel, I issue Blue Chip Buy Alerts when a top company falls to a historic buying opportunity.

Here’s some of the past results:

May 16, 2023 Buy Home Depot $240.50

Today Home Depot trades around $409 (+70%)July 18, 2024 Buy Bank of America $30.79

Today Bank of American trades around $39 (+26%)

Nike NKE 0.00%↑

Nike has dramatically underperformed the broader markets over the past several years. Year to date shares of the sneaker maker are down nearly 22%. Stretch it back to 5 years and shares have fallen 8%.

A series of missteps by outgoing CEO John Donahoe has left the brand falling flat with consumers and with retail partners.

That wasn’t surprising.

Mr. Donahoe had basically zero advertising and fashion experience before joining Nike. A rare misstep by founder Phil Knight and the board of directors for hiring him in the first place.

I’ve been calling for Nike to fire the CEO since earlier this year.

Luckily for you, it’s created a valuation in Nike that is a good entry point. With shares trading in the low 20’s TTM (trailing twelve months) Price to Earnings P/E - this has historically been a good time to buy the marketing giant.

Keep in mind however that Nike’s earnings are set to contract in the coming year, but more on the reasons for that later.

Fundamentally things should get better. As mentioned, CEO John Donahoe is leaving and Nike is bringing back Elliott Hill who began his career as an intern at Nike before retiring a senior leadership position in 2020.

I have a reliable contact who works at Nike, and he said the move was not only long overdue (as morale and motivation under Donahoe was clearly lacking) but also inspiring.

The fact Nike promoted a former intern who devoted his entire career to the company has him “pumped” to continue to work at Nike. He said other employees feel the same way.

Aside from John Donahoe’s clear misunderstanding of the fashion and marketing side of Nike, he did leave the company on very strong financial footing.

Despite negative revenue growth over the past year, Nike expanded gross margins and made necessary cuts on the staffing side.

Technically, Nike’s stock chart is a thing of beauty. Shares have just touched the bottom of a 30+ year uptrend.

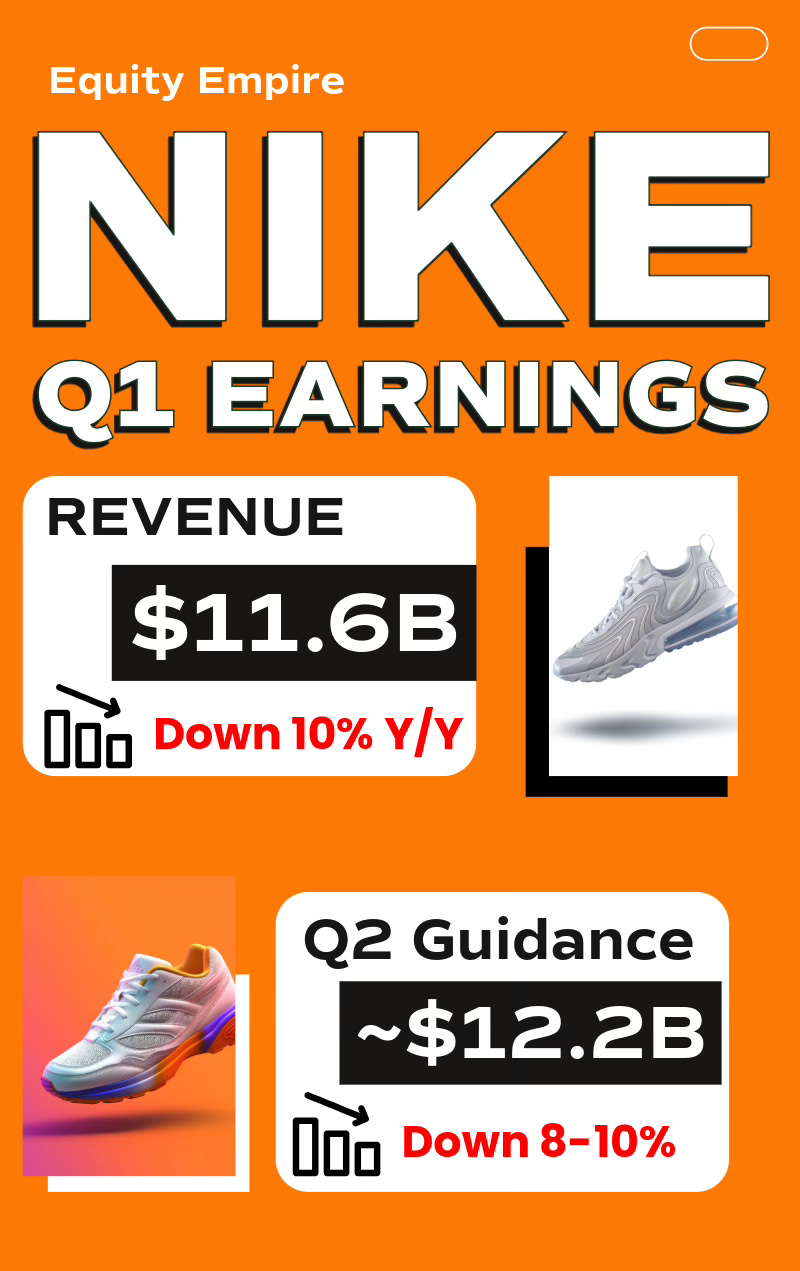

Q1 Earnings

On Tuesday Nike announced Q1 earnings.

They were a disaster.

Revenue was down year-over-year by 10% and the company indicated that Q2 (the holiday shopping quarter) would be down 8-10%.

Yikes!

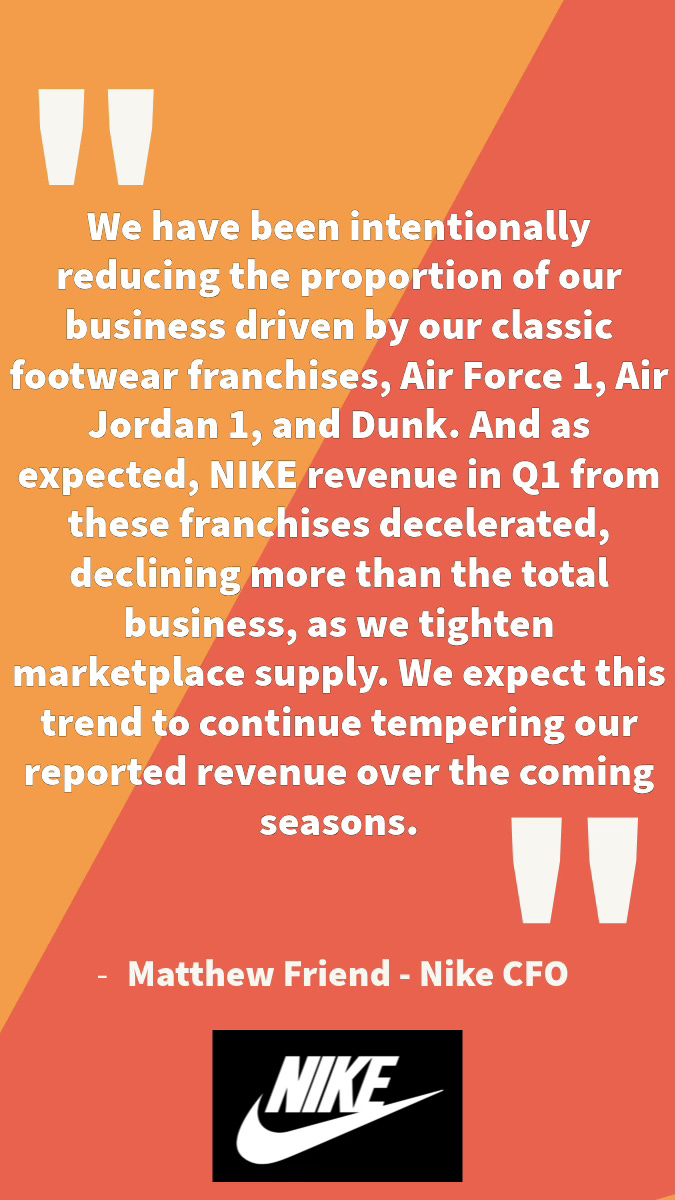

But the revenue miss is (partially) intentional.

Under previous CEO John Donahoe, the company flooded the marketplace with hot selling footwear including Air Force 1s, Air Jordan 1s, and low-top Dunk.

This is an amateur move that we’ve seen from brands like Under Armour in the past. A fashion company has a hot selling product and then all of a sudden it’s everywhere.

On the surface (and for investors) this may seem like a good thing, considering the revenue the sales bring in … and the perception that the brand is “popular”.

However, that’s not ideal for the brand long term.

Rolex, for example, is famous for under shipping demand on hot Rolex watch models. In fact, walk into a Rolex boutique and spread cash across the counter and they still won’t sell you a hot selling Daytona or GMT.

This has created strong secondary market demand for certain Rolex models that resell for more than the retail price.

The same was true for Nike for a significant portion of the high-end catalog. Shoes would be released and trade for more on the secondary market. That created an urgency and “hotness” for the brand.

Before John Donahoe, Nike would “slow drip” hot selling sneakers into the market. Initially there would be a “wave one” shipment that would intentionally undersell demand. That would create strong secondary market demand (hype) and maintain pricing for a “wave two” shipment.

During the Q1 conference call, Nike announced it is doing the correct (but difficult) thing for the brand and ultimately shareholders in the long run.

The company is intentionally underselling Air Force 1, Air Jordan and Dunk brands in order to create a better balance between supply and demand. That will impact Nike’s sales considering how popular these sneaker models have been.

Ultimately it will help Nike keep pricing high on these models when they do release, and create an urgency from consumers to buy them when available.

Competition

Lastly we’ll discuss competition. Former CEO John Donahoe was brought in to increase Nike’s direct to consumer sales.

He did that. But he over did it.

Nike severed relationships at retailers like Macy’s M 0.00%↑ and DSW. It drastically reduced shipments to Footlocker FL 0.00%↑ That forced those retailers to look elsewhere.

In particular, running brands Hoka DECK 0.00%↑ and On ONON 0.00%↑ have gained marketshare in running shoes.

Nike losing ground to competitors in a specific category is nothing new.

At one time Reebok had more sales than Nike.

Adidas was red hot after signing Kanye West.

Back in 2016 Under Armour UAA 0.00%↑ was red hot with Stephen Curry.

Nike responded recently by bringing back Tom Peddie who retired in 2020 as the company was phasing out its retail partners. This should help Nike gain back shelf space at retailers … or at the very least cause competition brands to pay more.

I actually view the competition aspect of Nike’s challenges as overblown. Reebok, Adidas and Under Armour have lost all momentum they had built up.

Hoka and On are largely competing in one category (running).

I would argue that the competition that Nike faces is the lowest it’s been in some time, given the struggles Under Armour, Adidas and certainly Reebok have faced.

Recommendation

Nike is a BUY.

The investment doesn’t come without risk. The main on would be a recession or “hard landing” of the United States economy. In that scenario your entire portfolio will get whacked - Nike wouldn’t be immune to that.

Downside protection. You would not want to see Nike shares trading below $69. Risk adverse investors should sell at that level.

Upside is a retest of the technical pattern above $180.

In other words, your downside risk is about $13 per share and upside is about $100 per share. These are the risk/reward setups that I look forward to bringing you here on the Newsletter.

Hope everything is well and look for another newsletter soon. If you could do me a favor and send this to a friend that would be great. Thanks again

Colin

Amazing!! Can’t wait for the paid subscription!