Natural Gas: The Unsung Hero Powering the AI Revolution

One executive called the opportunity a "Gold Rush" this month. Investors who spot this opportunity have the chance to stake their claim in this energy opportunity.

The artificial intelligence boom is reshaping the world.

But behind the scenes of every chatbot lies a less glamorous reality:

An insatiable demand for power.

AI data centers, with their armies of GPUs and cooling systems, are driving U.S. electricity consumption to unprecedented heights.

Berkeley Labs projects that potentially 12% of total U.S. demand by 2029 will come from data centers.

Renewables like solar and wind, while critical, can’t keep up with this exponential growth alone.

In fact, relying solely on renewable energy sources would put the United States at a disadvantage compared to countries like China.

Enter natural gas: reliable, scalable, and ready to bridge the gap.

One executive of a company we reveal to paid subscribers calls this moment a “Gold Rush”.

For investors, this isn’t just about keeping the lights on—it’s about spotting the companies and specific regions poised to capitalize on this energy goldmine.

Why Natural Gas? The Case for a Fossil Fuel Comeback

Natural gas is having a moment, and it’s not hard to see why.

AI data centers need dispatchable power—energy that can be turned on or off at a moment’s notice, unlike the intermittent nature of renewables.

Natural gas fits the bill perfectly.

It can ramp up in minutes, run at over 80% capacity, and scale to meet gigawatt-level demands.

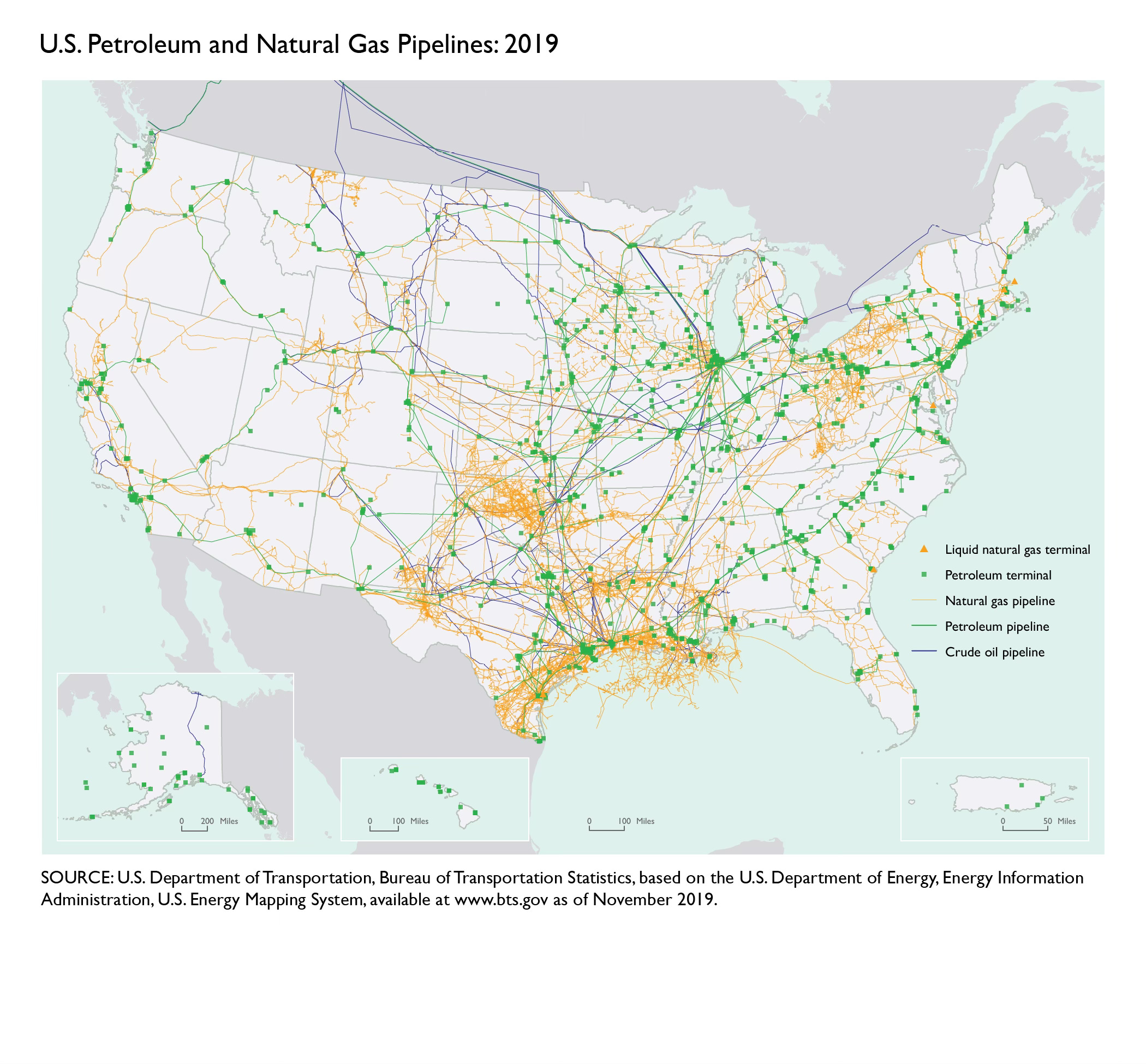

The U.S., as the world’s largest producer of dry natural gas, boasts a sprawling three-million-mile pipeline network, making it uniquely positioned to feed this hungry beast.

The numbers tell the story.

AI installations, powered by energy-hogging GPUs, can consume more power per task than traditional CPUs.

Cooling systems alone can eat up 40% of a data center’s energy.

Training models like ChatGPT-4 reportedly gulped 50 GWh (that’s 0.02% of the energy California generates in a year).

With McKinsey projecting AI to drive 70% of new data center capacity by 2030, the pressure on energy supply is relentless.

Natural gas, often dubbed the “cleanest” fossil fuel with 50% less CO2 emissions than coal, is the only viable option that can deploy quickly enough to meet this demand.

And speed is important here.

Rival countries like China have fewer power constraints.

For the United States to remain the leader in AI - quick access to power will be key.

Policy tailwinds are also in play.

The Trump administration’s push to fast-track natural gas projects.

Most investors are mistakenly focused on low-carbon solutions like small modular reactors (SMRs) or green hydrogen.

These projects are years - if not decades away.

Meanwhile, the data center industry is expanding at a rate that cannot wait for these technologies to be ready.

This is the moment natural gas cements its role as a “bridge fuel” to future low-carbon solutions like small modular reactors (SMRs) or green hydrogen.

The Technical Edge: How Natural Gas Powers AI

Let’s get into the nuts and bolts.

Natural gas powers AI data centers in two primary ways:

Grid-based solutions = where utilities lean on public gas-fired plants to supply electricity.

Off-grid solutions = where data centers directly tap gas via dedicated pipelines.

Both approaches are gaining traction, and each offers distinct opportunities for companies in the natural gas value chain.

Grid-Based Solutions: Utilities and Midstream Muscle

Utilities are racing to meet data center demand, with two-thirds of forecasted load growth in the Southeast tied to new facilities.

This is where midstream companies—those responsible for transporting, storing, and processing natural gas shine.

Analysts estimate data center demand could drive 3-6 billion cubic feet per day (bcf/d) of additional natural gas consumption by 2030, with some bullish forecasts hitting 10-12 bcf/d.

To put that in context, U.S. power sector gas demand was 35.4 bcf/d in 2023.

This incremental growth is a boon for midstream operators.

Companies like [REDACTED FOR PAID SUBSCRIBERS ONLY] are best positioned to benefit.

[REDACTED FOR PAID SUBSCRIBERS ONLY], for instance, is eyeing 4.5-5 GW of demand in the Southeast alone.

[REDACTED FOR PAID SUBSCRIBERS ONLY] has a strong foothold in Texas, a data center hotspot.

These firms are building shorter “lateral” pipelines—costing $15-50 million and completable in under a year—to connect directly to data centers or nearby power plants.

These projects sidestep permitting hurdles and community pushback, making them low-risk and high-reward.

Off-Grid Solutions: Direct Deals and Co-Location

Off-grid solutions are where things get innovative.

Cash rich data center operators, frustrated by grid constraints and permitting delays, are increasingly striking direct deals with gas producers or midstream firms.

For example, [REDACTED] AI data center secured [REDACTED FOR PAID SUBSCRIBERS ONLY] via a dedicated lateral pipeline.

This trend is particularly pronounced in gas-rich states like Texas, Louisiana, and the Midwest.

Texas, the top U.S. gas producer, offers tax breaks and robust infrastructure, making it a magnet for off-grid AI hubs.

Major players like [REDACTED FOR PAID SUBSCRIBERS ONLY] are jumping in, developing gas-fired plants with carbon capture technology to power data centers.

Even Microsoft MSFT 0.00%↑ despite its carbon-free goals, is open to gas with carbon capture if it’s cost-competitive, signaling a pragmatic shift among tech giants.

The Regional Play: Where to Watch

Geography matters. Northern Virginia, near the Marcellus Shale, and Dallas-Fort Worth, close to the Permian Basin, are ground zero for data center growth.

The Marcellus region produces 34.1 bcf/d but faces pipeline constraints, though the recently completed Mountain Valley Pipeline adds 2.5 bcf/d of capacity.

The Permian, meanwhile, is expected to ramp up to 11.9 bcf/d by 2038.

These regions favor midstream operators with existing assets, like [REDACTED FOR PAID SUBSCRIBERS ONLY], which connects Texas to the Northeast.

Smaller players like [REDACTED FOR PAID SUBSCRIBERS ONLY] could also see gains, particularly in Marcellus and Haynesville shale regions.

Investors should keep an eye on these nimble operators for potential upside.

Risks and the Road Ahead

Natural gas isn’t without challenges.

Overbuilding gas infrastructure risks stranded assets if data center demand underperforms, potentially burdening ratepayers.

Goldman Sachs estimates AI-driven gas use could add 200 million tons of CO2 emissions annually by 2030, clashing with tech companies’ zero-emission pledges.

Utilities like Dominion Energy D 0.00%↑ face scrutiny for aggressive capacity forecasts, and environmental groups like the Sierra Club warn of fossil fuel lock-in.

Yet, the industry is hedging its bets.

Natural gas is pitched as a bridge to SMRs (like Oklo’s OKLO 0.00%↑ planned 2027 deployment) or hydrogen, though both remain years away. For now, gas is the backbone of AI’s growth, and midstream companies are poised to ride the wave.

Investor Takeaway

Natural gas is no longer just a fossil fuel—it’s the linchpin of the AI revolution.

Midstream giants like [REDACTED FOR PAID SUBSCRIBERS ONLY] offer stability and contracted cash flows, while smaller players like [REDACTED FOR PAID SUBSCRIBERS ONLY] present growth potential.

Focus on firms with assets in Texas, Virginia, and the Southeast, where data center demand is hottest.

Watch for consolidation, as pipeline constraints make existing assets more valuable.

The AI boom is here, and natural gas is powering it.

For investors, this is a chance to back the infrastructure fueling the future—without betting on speculative tech. As always, do your due diligence, but don’t sleep on this quiet giant.

Follow Colin on social media: https://lnk.bio/equityempire