Retail Woes, Oil Slump, and Real Estate Risks - This Week’s Macro Insights

Today we look at the struggling Commercial Real Estate sector. Big Lots is the latest discount retailer to crumble under inflation. Crude Oil prices reflect a weak economy.

Happy Monday if that’s a thing. Every Monday here on the newsletter expect a Macro Monday Report.

I’ll try to consolidate the most interesting Macro news over the past week. The data will range from antidotal stuff I find interesting to more robust government data and trends.

Today we’ll look at struggling discount retailers. Commercial Real Estate set to bottom soon? Finally crude oil prices set to head lower.

The Antidotal

Big Lots BIG 0.00%↑ is set to file for bankruptcy. The discount retailer operates around 1,400 stores and has 30,000 employees. High debt was a factor, but the lack of operating profits ultimately took this retailer down.

This follows dismal results for other discount retailers including Dollar General DG 0.00%↑ and Five Below FIVE 0.00%↑ . Inflation has demolished the margins of discount retailers and the low-end consumer, which is unfortunate - but as investors this should create opportunity in the value retailer sector in 2025. Meanwhile the big-boys Target TGT 0.00%↑ , Walmart WMT 0.00%↑ and Costco COST 0.00%↑ should continue to gobble up marketshare.

Recommendation: Remain long TGT, WMT, COST. Be ready to rotate into the survivors once the dust settles.

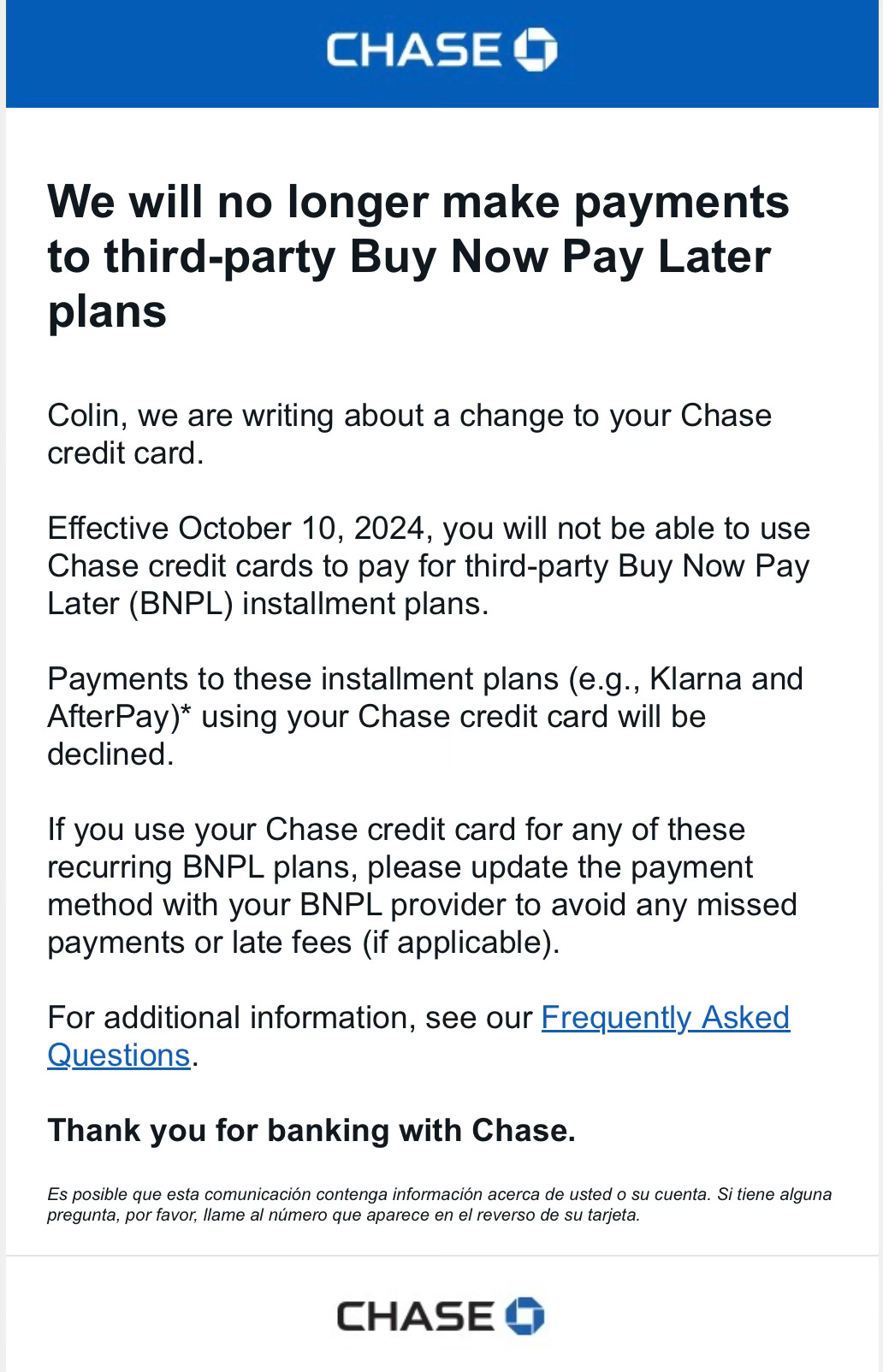

Got an interesting e-mail from Chase JPM 0.00%↑ this past week. The company will no longer allow users to pay for Buy Now Pay Later charges with a Chase credit card. Could be a push by Chase to get consumers to use its own service, but this is more likely a sign that Chase is witnessing a higher level of defaults from consumers using a Chase card to pay for BNPL services.

Crude Oil Plunge

If you drive a gasoline car, you’ve likely noticed the lower prices at the pump. And it’s likely going lower. Crude Oil futures are down over 10% just in the past month. OPEC+ responded by pausing a plan to increase supply by 180,000 barrels per day.

Economists are mixed on the reasons for the slide, but a weaker economy is only one source of lower demand. For the past two months Electric Vehicles accounted for more than 50% of the new vehicles sold in China. Some believe this is enough to knock down demand for oil exports into China.

Complicating the situation is the United States Presidential election in November. Almost nothing is certain from a policy standpoint - as the winning candidate would need control of both the House and Senate to pass any major legislation.

However, Former President Donald Trump could likely push Oil prices even lower as executive action can be a driving source opening up (even) more supply coming from the United States.

With the former President's chances of winning (at least) being a 50/50 possibility - (some) traders could be front running a potential return to office.

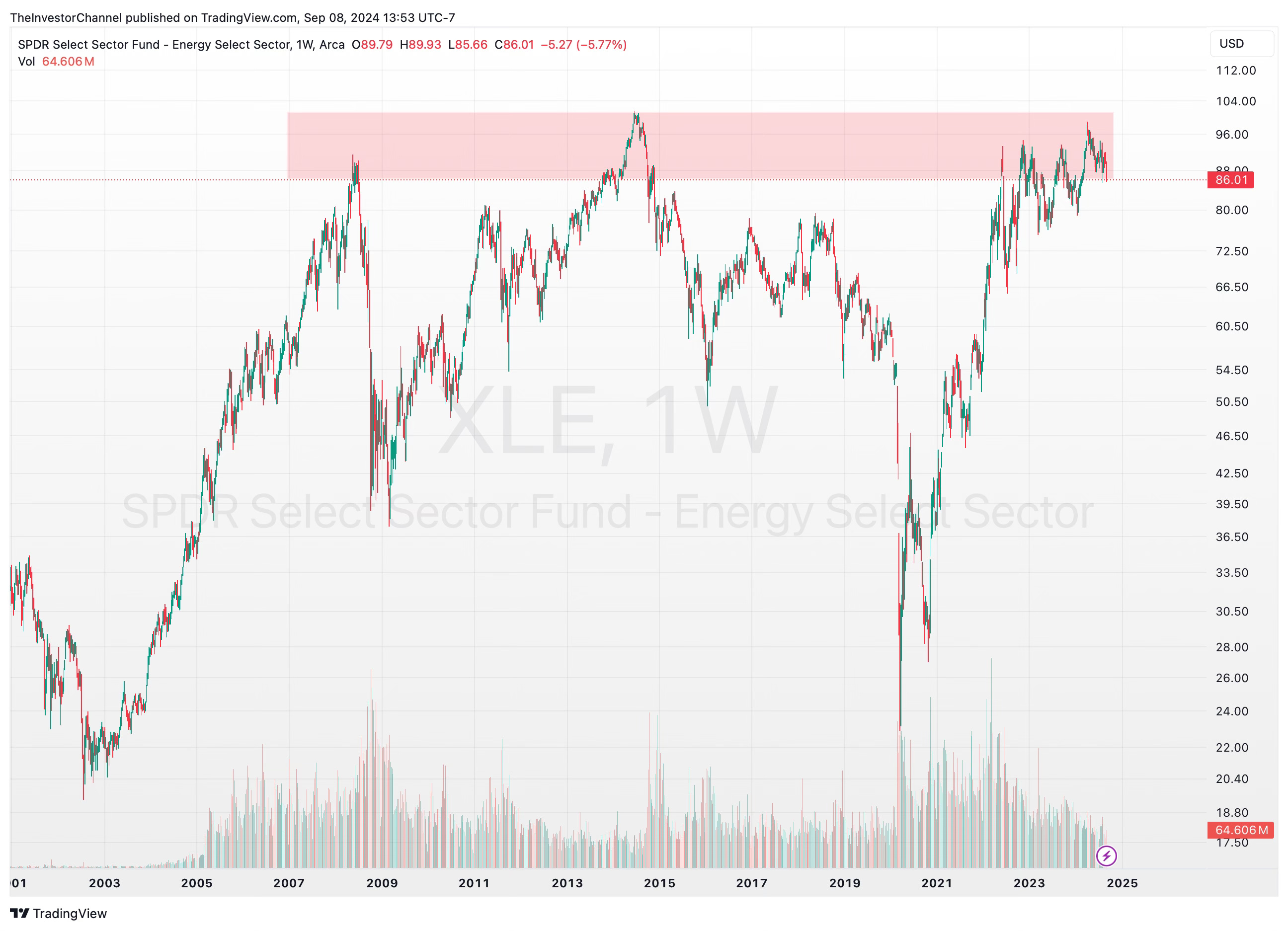

The XLE 0.00%↑ ETF - isn’t a true reflection of oil price, but will trade in parallel to the strength of oil prices appears poised to be rejected at a ~ $100 price level. This level has been a reversal area several times over the past 15+ years.

Takeaway:

Lower, crude oil pricing indicates a weak global economy. This echos the data we’re seeing in the job market and supports a FED rate cut later this month.

Recommendation: Underweight Oil until after 2024 US Elections. A Vice President Harris victory could present a buying opportunity.

Commercial Real Estate (CRE)

I’ve read lots of commentary about the commercial real estate sector since the pandemic. While a “return to office” has picked up a little, office vacancy still remains elevated in every major market.

S&P Global projects $950B in commercial real estate loans will mature and 2024, with 2027 serving as a peak with over 1.25T coming due. These loans will need to be refinanced, which will put pressure on the banks that hold the existing loans.

Moody’s feels the office market could be approaching the bottom as transaction volumes are leveling off. More interestingly, several high profile office buildings have been sold at eye-popping $100M+ loses. Moody’s believes this price discovery of distressed properties could allow banks to better asses risk going forward.

The 3 large banks JP Morgan JPM 0.00%↑ Wells Fargo WFC 0.00%↑ and Bank of America BAC 0.00%↑ all have significant exposure to the sector both on the office side and multifamily apartment side.

The eye-popping loses are requiring the large banks to write down assets and set aside loan-loss reserves for potential defaults. While Moody’s believes this is marking a bottom, the elevated vacancy rates lead me to believe the office sectors is not close to recovery.

None of this has mattered much to the financial sector however. The XLF 0.00%↑ ETF is in a well defined uptrend and has just achieved a fresh all-time high.

Takeaway:

I’ve been taking profits on the two banks stocks I own JPM 0.00%↑ and BAC 0.00%↑. Both stocks have outperformed the broader markets over the past year with JPM up over 46% and BAC up over 36%. With Warren Buffett selling around 16% of his BAC shares, I’ll take that as a sign that the risk is to the downside.

Rate hikes were good for banks over the past year, I believe the next cycle lower will mitigate some of the stress in the CRE market, but not enough to propel the sector higher.

Recommendation: Take profits on financial stocks that have run over the past year. Remain underweight Financials.

Conclusions

The cumulative impact of inflation and “higher” rates is showing up across a wide range of macroeconomic data.

The mainstream “macro doom” pundits will use all the negative data points to predict recessions across the globe.

I believe it’s too early to draw those conclusions.

But some things are clear.

The underlying weakness won’t be instantly solved by a quarter point rate cut. Poorly run businesses and office buildings are going to be in distress. Don’t make the mistake of throwing out the good with the bad. Well run companies should continue to thrive.

That’s it for today, see you later in the week.

Colin

Great Information