Why Nvidia’s Stock Could Keep Climbing: Analyzing Blackwell Chip Demand and Market Projections

Is Nvidia Still a Buy? Unpacking the Wild Revenue Estimates from Wall Street

If you've been following my weekly YouTube show on the semiconductor industry, you're aware that something unusual is going on with Nvidia.

The semiconductor giant has been one of the top-performing stocks in recent years, propelling Nvidia into the ranks of the world's most valuable companies.

With this increased market cap comes heightened attention and scrutiny.

However, unlike other mega-sized tech firms, Wall Street still can't quite figure Nvidia out.

Today I will discuss something highly unusual about Nvidia stock and unlock some clues to why the stock could still be a buy - even after it’s epic 2,800% run higher over the past 5 years.

First we have to understand how Wall Street operates.

As you know companies report earnings each quarter.

In the press release companies usually highlight revenue, revenue growth over the previous year and earnings per share or EPS.

Most companies often provide forward guidance to these data points for the upcoming quarter. In my experience, it’s the forward guidance which can move the stock the most.

All of these data points have a measuring stick.

The measuring stick Wall Street uses are estimates from industry analysts at large research firms like Goldman Sachs, UBS, Mizuho, Citigroup, Wedbush, among others.

Typically companies the size of Nvidia have 20+ analysts making predictions on where revenue and earnings will fall over the next several quarters.

This is where things get interesting.

Large companies with dozens of analysts rarely deliver surprises.

Think of it this way: in sports, predictions about athletes' performances are constantly being made, whether for fantasy football leagues or sports betting.

When it comes to elite athletes, their performance tends to be consistent and fairly predictable. It’s uncommon for a top athlete to deviate significantly from expectations.

The same could be said about elite publicly traded companies.

Outside of an unplanned event (like a pandemic or hurricane for example) large companies tend to fall within the range of expectations set forth by Wall Street.

Take for example Apple AAPL 0.00%↑ .

Just like Nvidia the company has about two dozen analysts predicting its revenue trend over the next year.

It would be highly unusual if the spread between the low-end estimate and high-end estimate was really wide.

In other words … the expectations for Apple are pretty much agreed upon in advance.

Looking forward there’s at most a 13% gap between the high and low estimates for the companies revenue as seen below.

Pull up the revenue estimates of any megacap company and the estimates put forth by Wall Street analysts will almost always be within a fairly tight range.

Going forward if Apple can have revenue come in towards the high-end revenue estimates, the stock will likely perform very well.

This is where things get interesting for Nvidia.

That’s because unlike Apple and virtually every megacap company I’m following - the revenue estimates for Nvidia are dramatically different.

That means Wall Street has no idea how much revenue Nvidia will generate in the coming few quarters.

I’ll talk about the clues that indicate which direction Nvidia revenues are likely to come in, but let’s first look at the wildly different views Wall Street analysts have about Nvidia’s earnings.

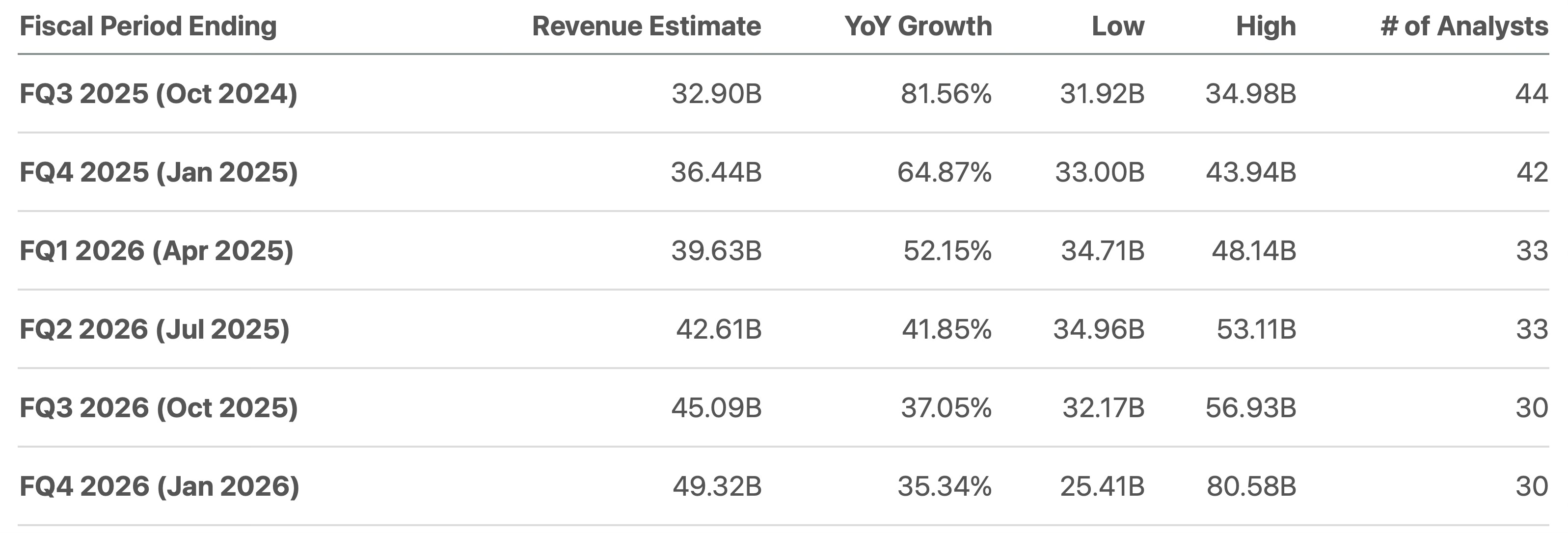

First notice that the upcoming quarter FQ3 2025 for Nvidia falls within a tight range. The low-end estimate is for $31.92B and the high-end estimate is for $34.98B.

This is largely because Nvidia provides forward revenue guidance for 1 quarter when the company reports earnings.

When Nvidia reported Q2 earnings back in August, the company said Q3 revenue would likely come in at $32.5B +/- 2%.

Hence the reason why Wall Street analysts have congregated around a $32.5B revenue estimate for the Q3 given that is what Nvidia indicated just a few months ago.

But after that is where things get far more interesting.

Just one quarter forward Wall Street analysts are very far apart on Nvidia’s revenue potential. With the low-end estimate being $33B and the high-end coming in at $43.94B!

That’s a 28.4% difference!

Notice that going forward the spread between the low-end estimate and high-end gets even wider. Looking forward to Q4 of 2026 the gap is 104%!!

That would be like one sports pundit saying the Super Bowl champion Kansas City chiefs will be 17-0 and another saying they will be 0-17. It really doesn’t happen very often.

So what does this all mean?

In short, depending on where Nvidia revenue comes in over the next few quarters will have a dramatic impact on the stock price.

Because we know Nvidia’s gross and operating margins are extraordinarily high … obviously higher revenue will equate to higher earnings.

If Nvidia is able to achieve revenue totals that are closer to the high-end - Nvidia’s stock is dramatically undervalued. And consequently if the low-end estimates are closer to reality, Nvidia share price will (at the very least) have a difficult time going higher.

The good news is we have plenty of anecdotal evidence that Nvidia’s revenue will be extremely strong over the next few quarters.

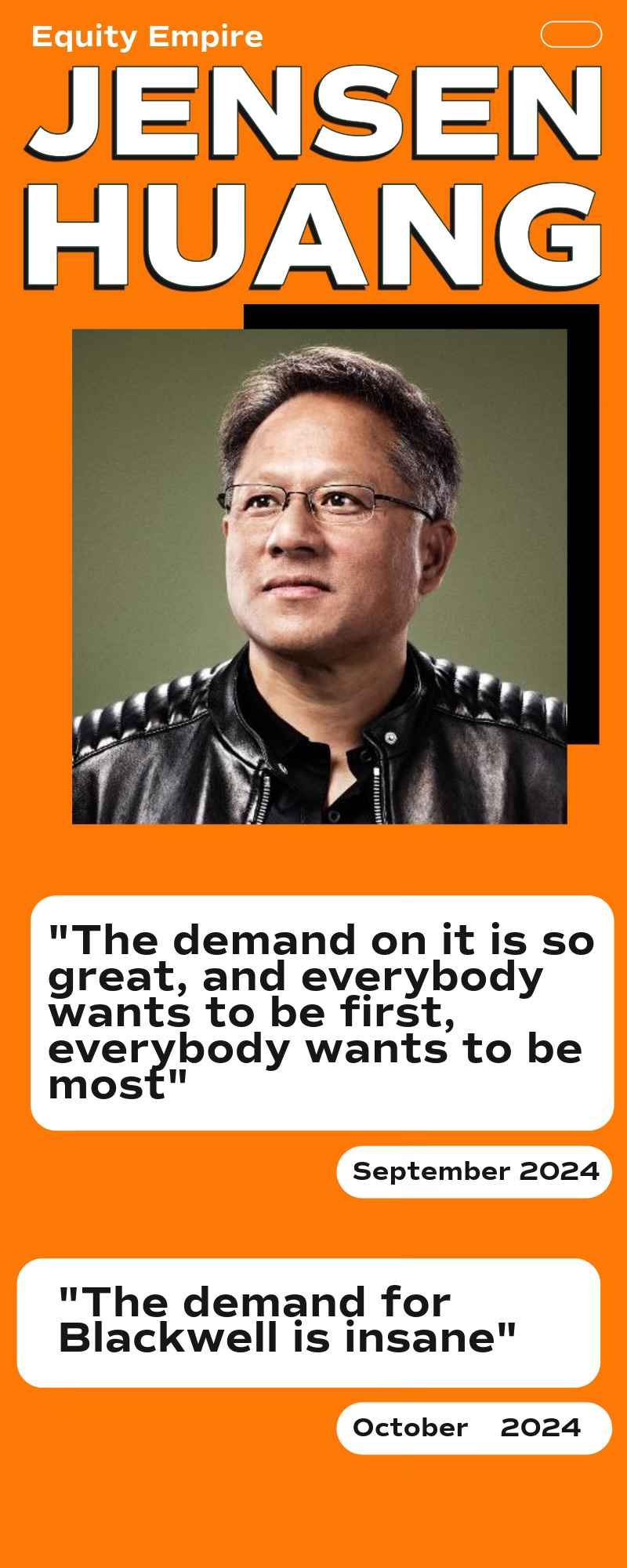

First, you have the CEO Jensen Huang himself talking up the company’s forthcoming Blackwell GPU.

The Blackwell chip will be critical to driving Nvidia’s revenue higher in the coming few quarters.

There’s no one outside the CFO of Nvidia who has a better view of forward demand than Jensen Huang.

Multiple times over the past few months he’s emphasized how “insane” the demand for the forthcoming Blackwell chip will be.

Part of the challenge for Nvidia is not selling Blackwell chips. In fact, most companies would buy as many as Nvidia is willing to sell them.

It was reported recently that Elon Musk and Larry Ellison (founder of Oracle) had dinner with Jensen Huang “begging” him to sell them more of Nvidia’s products.

The bottle neck for Nvidia is not demand, but it’s supply. For that the company relies on a wide web of suppliers including Taiwan Semiconductor Manufacturer TSM 0.00%↑ and SK Hynix for memory.

In October TSM announced its revenue increased 39.6% year-over-year - a good sign that the exclusive manufacturer of Nvidia’s Blackwell GPUs is (at the very least) seeing high demand.

In September memory supplier SK Hynix announced mass manufacturing of High-Bandwidth Memory (HBM) that will ship on board the new Nvidia Blackwell GPUs.

And finally, after reports that Blackwell manufacturing was delayed, Morgan Stanley reported that manufacturing ramp appears to be quite strong.

As these headlines have trickled in, Nvidia shares have quietly climbed over 20% over the past month.

That’s because Wall Street investors know exactly what I’ve outlined here.

If the company can have its manufacturing suppliers deliver Blackwell … the company has near limitless demand for the product in the short run.

My belief is Nvidia will come much closer to the high-end revenue estimates than the low-end over the next several quarters. That means that Nvidia shares, despite the rapid rise … is still a buy.

Make sure you tune into the Semiconductor Show - as I cover more than a dozen semiconductor stocks on a weekly basis.

Keep in mind I am long Nvidia shares.

Thanks, and hope things are good. See you again soon here on the Newsletter.

Colin